Factor Investor Report - September 2023

All things factor investing

This quarter has been a excellent quarter for mid and small cap stocks. Some funds were caught on the wrong foot as sector or companies they had specifically avoided did very well. The mid and small cap indexes and most systematic strategies with minimum sector bias however had exposure to those sectors. Interest rates globally are high and may continue to remain so for the foreseeable future. The US Central Bank is not in a mood to back off so quickly especially when the US economy and equity markets are quite resilient. Bond markets are however, in a tizzy. This backdrop makes for a very interesting last quarter for the calendar year. Until next year then.

- Editor

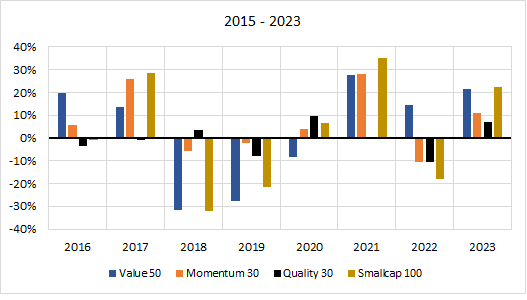

1. Factor Performance Summary

This quarter the universe of stocks made a big difference. While Momentum 30 generated a return of 9% for the quarter has Nifty 200 as its universe, Nifty Alpha 50 and Nifty Midcap Momentum 50, gave returns of 17% and 16% respectively for the quarter which was close to what Value 50 and the Smallcap 100 index returned. The Nifty 100 Alpha 30 index, which has largecap as its universe gave a return of 5% for the quarter.

Even for the YTD Nifty Midcap Momentum 50 gave a return of 31% which is inline with what the Smallcap 100 and Value 50 indices returned. In contrast Nifty 100 Alpha 30 was flat for the year.

2. Tactical Asset Allocation

3. Relative Returns and Risk and Returns- Annual

4. Factor Ranks

Small and midcaps have had an excellent 6 months while the large caps have lagged. This is evident in the performance of smallcap index as well as the value index.

5. Factor Excess Return Correlations

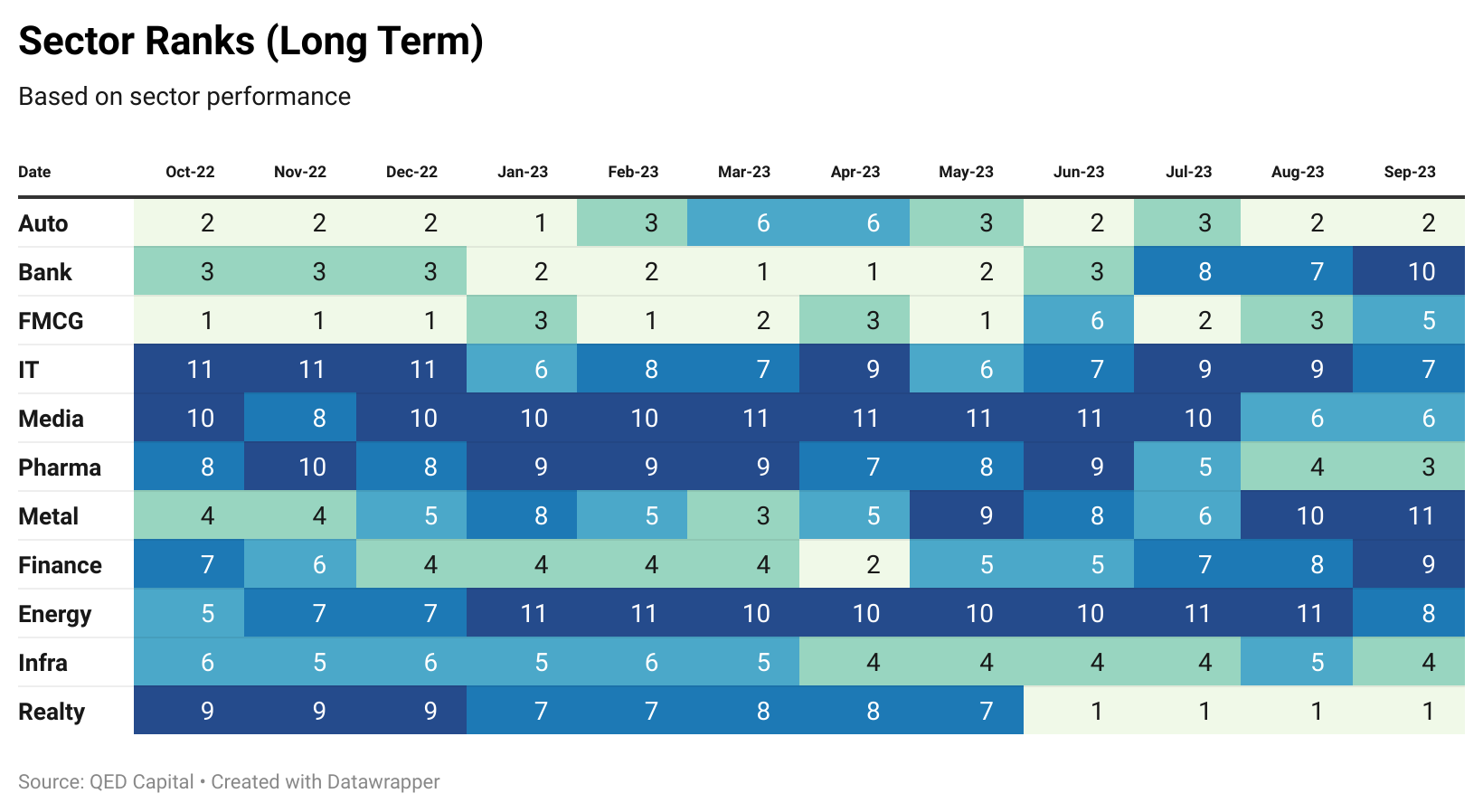

6. Sector Ranks

Realty has been the top performing sector for the 4th month in a row followed by auto and pharma. Banking and Finance remain laggards.

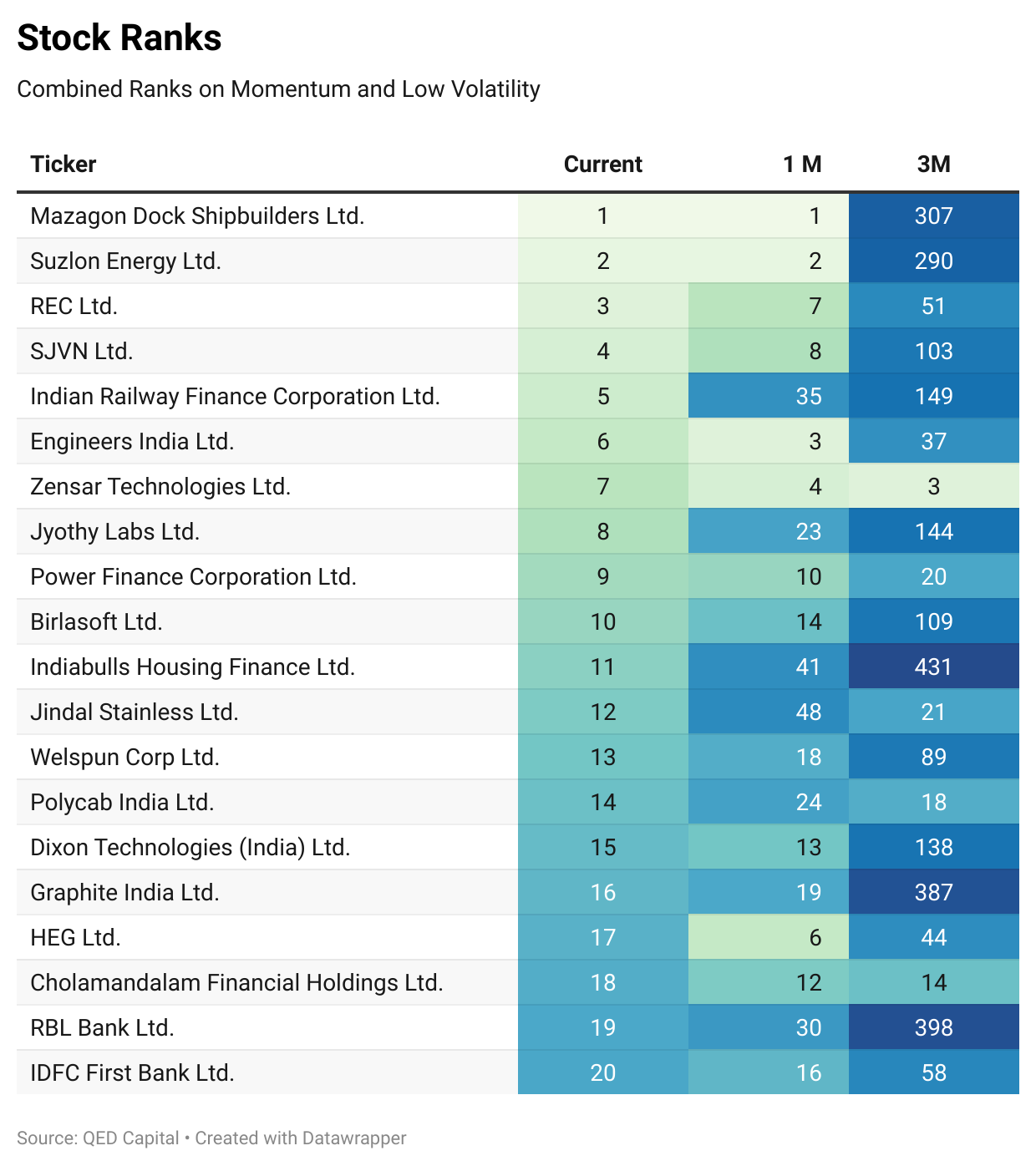

7. Stock Ranks

An important component of our process is ranking stocks on Momentum and Low Volatility over a look back period of 6 months. In the table below we show the top ranked 20 stocks in our Mid and Small Cap universe. The rank is a combined score of Momentum and Low Volatility. It also shows the ranking of the stock one and three months ago.

8. Readings

The 52-Week High Effect and Momentum Investing: Evidence from India by Rajan Raju

Using a dataset from October 2004 to August 2023, we employ various portfolio construction frameworks to show that the 52-week high effect is a distinct and robust phenomenon in the Indian equity market. This study investigates the predictive power of this phenomenon and contrasts it with academic momentum. We find that stocks near their past 52 weeks tend to offer higher returns and Sharpe ratio, even after controlling for firm size. Our findings are statistically significant and valid across various weighting schemes, reaffirming that the 52-week high effect is a distinct and robust market ``anomaly'', offering a more stable alpha than academic momentum in Indian equity markets. Furthermore, we find that 52-week high strategies have weaker long-term reversals relative to academic momentum, offering actionable insights for investment managers looking to capitalize on momentum-based anomalies. These findings suggest different underlying market responses to news for the two effects and provide actionable insights for portfolio managers and investors.

Disclaimer: Nothing in this blog should be construed as investment advice. This is purely for educational purposes only. Please consult an investment advisor before investing.