Factor Investor Report - October 2022

All things factor investing

We are excited to bring you the new and revamped Factor Investor Report. When we started this , we were not sure how many readers would be interested. However, over time, factor investing (smart beta to most) has picked up in India and now we have over 1200 subscribers. Our mission is to make investors aware about factor investing. It is a unique lens to view markets, from what tradition investors are used to. It is not very different from traditional discretionary investing though. As Transtend, a large European trend following investor put it, “ If you compare a good discretionary trader with a good systematic trader, then about 98% of their DNA should be similar too.” Do write in to us with your comments and feedback and spread the word about factor investing. We will be doing a video also every month with a commentary on the factor investor report.

- Editor

1. Factor Performance Summary

Value and High Beta made a big come back this month. Followed by the broader Market Factor.

Year to date numbers have to be read with a pinch of salt. The outperformance of the Growth index is not surprising given that India has remained a strong market in light of the global storm. Even US Markets are showing a rotation from Value to Growth. Growth is followed by Value and High Beta. Equal Weight (EW) has done slightly better than the broader market which is expected given that EW has a bias towards value. Small Caps have had a tough ride, but not unexpected given the super run they have post Covid.

2. Five Year Risk & Return - Absolute

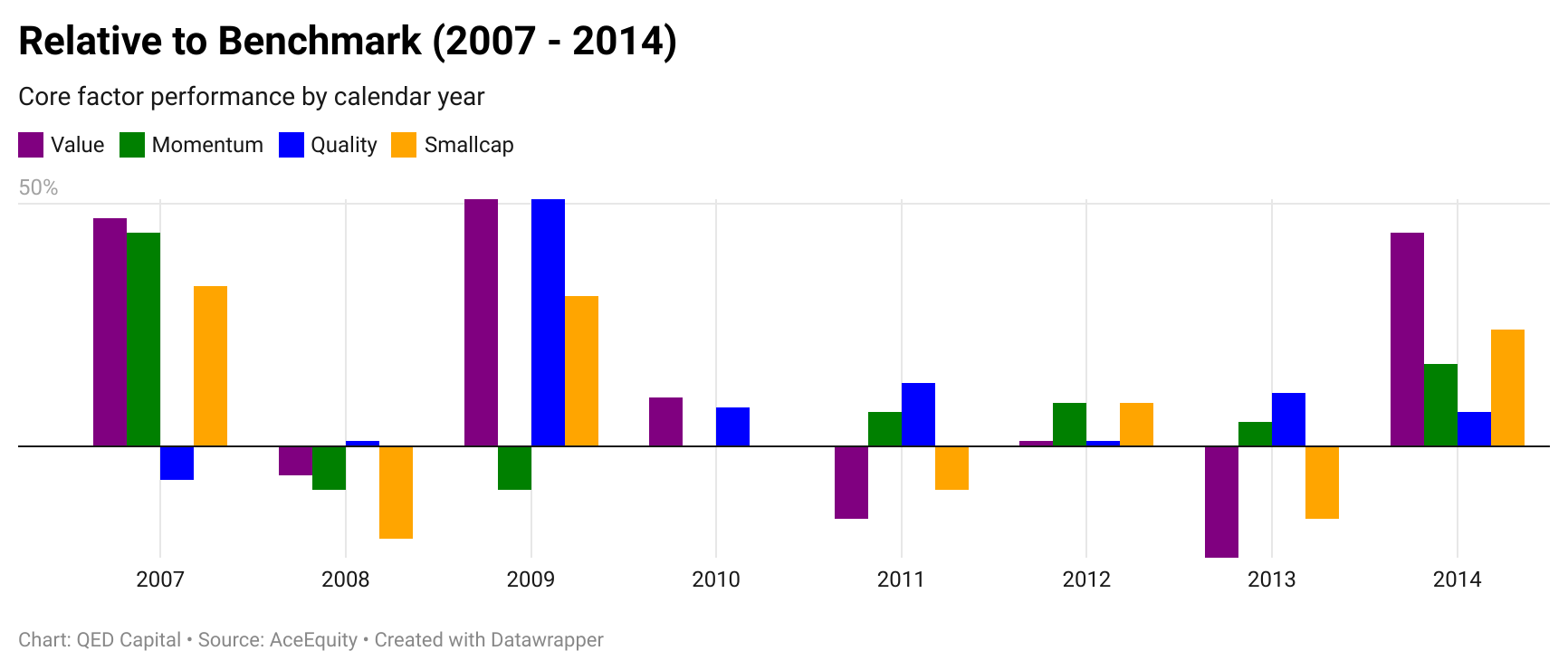

3. Relative Returns - Annual

4. Factor Ranks

Low Volatility makes a jump from 3rd place to the top rank. Followed by Value and Market. Not much change elsewhere in the table. Small caps continue to be the laggards.

5. Factor Excess Return Correlations

This is a key table. It explains how different factors can be used to construct a diversified factor portfolio of uncorrelated or less correlated factors. Correlations do change but some are quite robust and tend to snap back to long term averages. When one examines the parameters used to construct the factors, the relationships become quite intuitive and logical.

Value has high negative correlation with Quality and Low Volatility. It also has negative correlation with Momentum. Value has very high correlation with High Beta. So if one were building a portfolio of factors, value and quality would be good diversifiers. Globally, Value and Momentum have shown to have low and negative correlation across long periods.

Most investors confuse Momentum with Growth investing. This table shows Momentum has a negative correlation with Growth, which should confound them even further. Factor investors however, know that Momentum and Growth investing are very distinct.

Low Volatility has a high correlation with Quality and Dividend.

6. Sector Ranks

FMCG is at the top spot followed by Auto which falls a rank. Banks and Metals gain a rank. IT, and Pharma continue to lag.

7. Stock Ranks

An important component of our process is ranking stocks on Momentum and Low Volatility over a look back period of 6 months. In the table below we show the top ranked 20 stocks in our Mid and Small Cap universe. The rank is a combined score of Momentum and Low Volatility. It also shows the ranking of the stock one and three months ago.

Disclaimer: Nothing in this blog should be construed as investment advice. This is purely for educational purposes only. Please consult an investment advisor before investing.