Factor Investor Report - Jun 2025

All things factor investing

A roller coaster ride for the first six months for smallcaps with very little to show for while large caps have returns in the high single digits. That is not a bad outcome given the geo-political and macro economic events that markets have been through. Banking and Finance sector led from the front with other sectors following.

After a cautious March quarter shaped by global trade tensions and geopolitical uncertainty, the June quarter brought signs of improving sentiment. Trump Tariffs were top of mind for markets globally. Locally we went through a short war with Pakistan and a mixed earnings season.

This quarter, the bulls were back — led by banks and armed by defence. Risk led the charge, but under the surface, investors still leaned on caution over conviction. Rate cuts were front loaded by the RBI and policy stance moved to neutral from accommodative.

Sector participation widened, and capital rotated into pockets of the market that had lagged earlier in the year. While the rally was broad, it wasn’t driven by trend-chasing — it reflected a reset in positioning, as investors began unwinding defensive bias without fully letting go of restraint.

- Editor

1. Factor Performance Summary

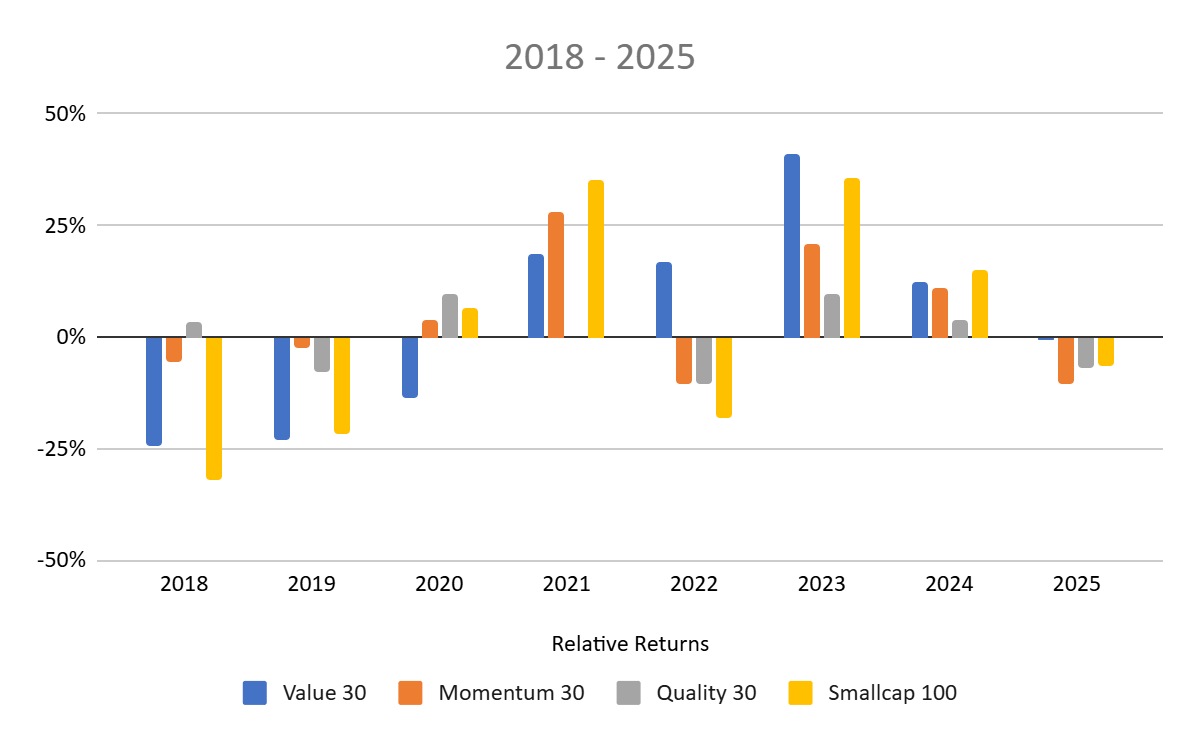

The June quarter saw a sharp reversal in factor performance. Smallcap, High Beta, and Momentum—all of which were the weakest performers in the March quarter—led the recovery.

Low Volatility and Value, which had held up during the March drawdown, also posted solid gains in the rebound, though they trailed the more aggressive factor cohorts and the market. Equal Weight delivered steady returns across both quarters, pointing to broad participation beyond just extremes.

The shift reflects a move from defensive caution to tactical risk-taking, as positioning adjusted to evolving macro clarity and the fading of early-year overhangs.

2. Tactical Asset Allocation

3. Relative Returns and Risk and Returns- Annual

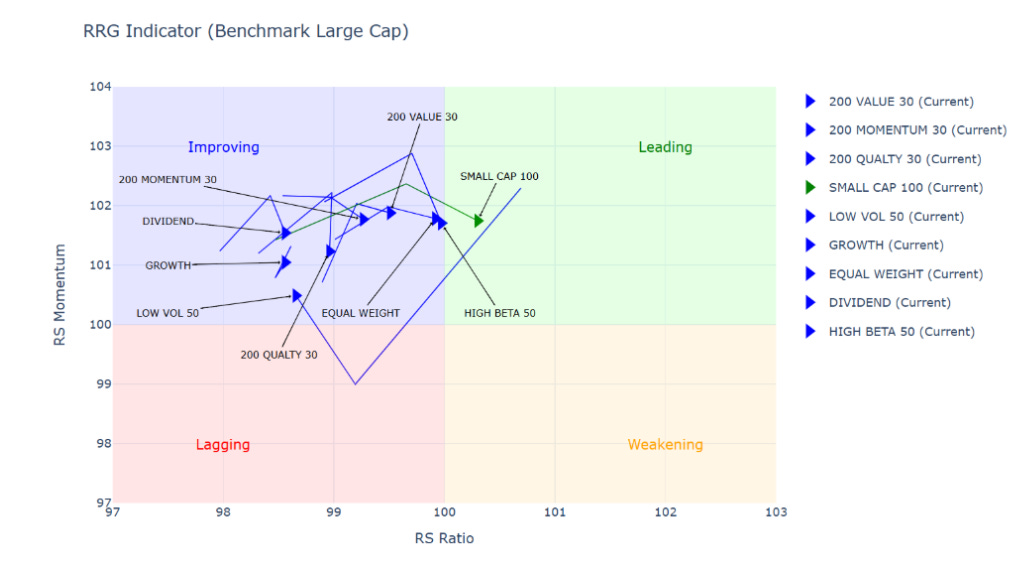

4. Factor Ranks

The long-term factor ranks show a market still anchored in caution. Low Volatility remained among the top-ranked factors through most of H1 2025, suggesting that even as equities rallied, investors preferred stability over speed. Its consistent leadership reflects persistent demand for defensiveness — a likely result of slow earnings and macro uncertainty.

At the same time, Momentum has remained bottom-ranked for six straight months, despite its strong June-quarter return. This points to a lack of sustained trends and reflects how previous underperformance continues to weigh on its composite signal.

Market and SmallCap have gained ground in recent months — the former holding a top-2 rank since February and the latter jumping to number 1 in June — signaling a measured return of risk appetite, but not a wholesale shift in regime.

Meanwhile, Value, Quality, and AlphaLowVol have stayed mid-pack, reinforcing the sense that no single style has dominated outside of Low Vol, and that investor conviction remains somewhat uncertain.

5. Factor Excess Return Correlations

6. Sector Ranks

Finance has emerged as the most consistent outperformer, holding the number 1 rank for four straight months and staying in the top 3 since December. Banks, too, have steadily climbed the ladder — ranked number 2 since April — reflecting sustained strength in financials across the board. This leadership aligns with strong liquidity conditions, policy tailwinds, and renewed institutional positioning.

Metals and Infra have shown notable improvement in recent months, both rising steadily into the top 4 by June. Their rise points to growing risk appetite and participation in cyclical, capex-linked themes.

Pharma, after a strong stretch from late 2024 into early 2025, has cooled slightly but remains well ranked — a sign that defensive exposure still finds favour in uncertain periods.

IT, after peaking in Jan–Feb, has fallen sharply and now ranks mid-pack, reflecting a lack of trend clarity in global-facing names.

7. Stock Ranks

An important component of our process is ranking stocks on Risk Adjusted Momentum over a look back period of 6 months. In the table below we show the top ranked 20 stocks in our Mid and Small Cap universe. The rank is based on Risk Adjusted Momentum score. It also shows the ranking of the stock one and three months ago

8. Readings

Should Investors Combine or Separate Their Factor Exposures?

by Jose Ordonez, Alpha Architect

The answer depends on your goals and preferences.

The integrated approach makes sense for investors running long-short portfolios, where avoiding contradictory positions is crucial. It also suits those seeking exposure to multiple (or most) investment factors—such as value, momentum, size, quality, and

The mixed approach, on the other hand, may be better for investors who are less concerned about tracking error and more focused on maximizing expected returns. It also allows for cleaner attribution of returns and provides more behavioral clarity, making it a great strategy for those wishing to understand what’s driving portfolio performance.

Disclaimer: Nothing in this blog should be construed as investment advice. This is purely for educational purposes only. Please consult an investment advisor before investing.