Factor Investor Report - December 2022

All things factor investing

After a horrible decade, the last two years have seen a huge comeback for Value factor. This year too, Value beat Momentum and all other factors. The underperformance of other Momentum when Value is doing well is not surprising given that Value and Momentum are least correlated factors. Also as we will talk about more that in the coming issues, given that factor definitions matter a lot. Momentum, is affected a lot by its rebalance period. The current version we are tracking has a six month rebalance period. If we were tracking a faster rebalance momentum index, the performance might have been better. However, Value would have still outperformed, only the out performance would have been a bit less.

Wishing you all a very happy new year!!

- Editor

1. Factor Performance Summary

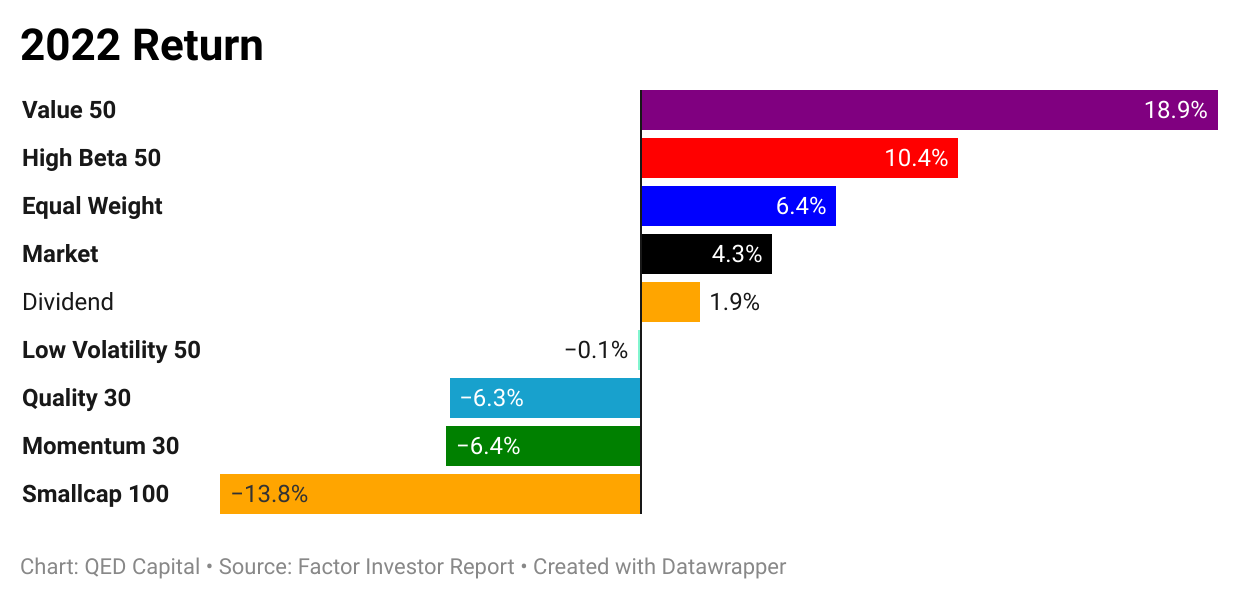

In a month where all other long only factors were negative, Value delivered a positive return.

Value and its cousin, High Beta, end the year with double digit gains. Market and Dividend eke out single digit returns with the rest of the Factor family ending flat or negative. Small Caps (Size) were at the bottom with a loss of approximately 13%.

2. Five Year Risk & Return - Absolute

This chart, which we update every month, reminds us not to fuss too much over monthly and even annual returns. On a 5 year basis nothing much has changed. But if all investors understood that and behaved rationally, factors perhaps, would not work over time.

3. Relative Returns - Annual

4. Factor Ranks

Value continued its out performance though out the year. There was a brief period in middle of the year, when it suffered a stutter but then made a smart recovery in August to end the year at number one spot again. Market Factor has been the bulwark and held up the large caps. Low Volatility picked up during middle of the year. This may be due to the PSU pack picking up which includes a number of utility stocks. Quality and Momentum have not had a great year. Small Cap has been a back bencher for most of the year.

5. Factor Excess Return Correlations

Correlations guide us on how to construct a multifactor portfolio. The very first line tells us the story of the year. Value has a high correlation with High Beta and Equal Weight Market index. Both have done well. It has a negative correlation with Quality and Momentum. So if one had a multifactor portfolio, it would have been a decent year overall. It would not have been a great year for those who focus on single factors unless that factor was Value.

6. Sector Ranks

Value has been driven by Banking, Energy and Metals through the year. Banking picked up steam towards the end of the year and picked up the slack left by Metals and Energy. Energy had a great 9 months while Metals were a bit volatile.

7. Stock Ranks

An important component of our process is ranking stocks on Momentum and Low Volatility over a look back period of 6 months. In the table below we show the top ranked 20 stocks in our Mid and Small Cap universe. The rank is a combined score of Momentum and Low Volatility. It also shows the ranking of the stock one and three months ago.

8. Readings

Abstract: Monthly rebalanced, equal-weighted, long-only winner portfolios, drawn from the top 200 stocks in India, built using systematic rules that underpin popular factors of momentum, low volatility and quality deliver alpha for the period under study. The market exposure is significant across all the style strategies we looked at. Therefore, correlations between the strategies are significantly higher than those observed for academic factor returns. We include alternate calculation methodologies for some factors and find that not all implementations of factor strategies are the same. Not all strategies have high turnover. Indeed, strategies like low volatility and quality show fairly low turnover. Factor exposure persistence over time varies across strategies and persistence should be considered when implementing factor-style strategies. We also find that size and sectoral preferences of factors are dynamic and could reduce perceived diversification benefits. Finally, we show that alpha for momentum, low volatility and quality strategies survives real-world implementation costs. While winner portfolios using momentum, low volatility, and quality rank higher than the broad S&P 200 Index over the period under study, there is not one factor-style that is a consistent winner.

Link: https://ssrn.com/abstract=4000418 or http://dx.doi.org/10.2139/ssrn.4000418

Disclaimer: Nothing in this blog should be construed as investment advice. This is purely for educational purposes only. Please consult an investment advisor before investing.